Where to Buy Property Investments in Wells: Yields of 3.7%

Gross rental yields of 3.7% and asking prices averaging £364,636 across just two postcodes make Wells one of the most supply-constrained buy-to-let markets in the South West. Wells is a city in Somerset, South West England, and with a population of around 12,000 it is England's smallest city. Average sold prices in Somerset sit 4.6% below the England average at £278,440, and the former Mendip district's population grew 6.2% to 116,089 between the 2011 and 2021 censuses.

Somerset's average sold price of £278,440 positions the county below both the England average of £291,865 and the South West regional average of £301,226. That gap narrows when you look at Wells specifically. Asking prices of £350,472 in BA4 and £378,800 in BA5 sit above the Somerset sold price average, reflecting the premium that a cathedral city with limited housing stock commands. Rental data is available for both postcodes.

This guide covers the two postcodes serving Wells and its surrounding area: BA4 (Shepton Mallet) and BA5 (Wells). Wells falls within Somerset Council (ONS code E06000066), formed in April 2023 from the merger of the former district councils and county council. Investors comparing options in the region may also consider Bath, Bristol, Exeter, or Salisbury. Browse all our South West location guides.

Article updated: March 2026

Wells Buy-to-Let Market Overview 2026

Wells is a heritage micro-market where limited supply and lifestyle demand keep prices above the Somerset average, while yields remain modest by national standards.

- Average sold price: £278,440 (4.6% below England's £291,865)

- Asking price range: £350,472 (BA4) to £378,800 (BA5)

- Rental yields: 3.5% (BA4) to 3.7% (BA5) across both postcodes

- Rental income: Monthly rents from £1,020 (BA4) to £1,152 (BA5)

- Price per sq ft: House prices from £304/sq ft (BA4) to £342/sq ft (BA5)

- Market activity: Sales ranging from 17 per month (BA4) to 22 per month (BA5)

- Deposit requirements: 30% deposits range from £105,141 (BA4) to £113,640 (BA5)

- Affordability ratios: Property prices from 9.7 to 10.4 times Somerset's median annual salary of £36,279

Contents

-

by Robert Jones, Founder of Property Investments UK

With two decades in UK property, Rob has been investing in buy-to-let since 2005, and uses property data to develop tools for property market analysis.

Property Data Sources

Our location guide relies on diverse, authoritative datasets including:

- HM Land Registry UK House Price Index

- Ministry of Housing, Communities and Local Government

- Ordnance Survey Data Hub

- Propertydata.co.uk

We update our property data quarterly to ensure accuracy. Last update: March 2026. All data is presented as provided by our sources without adjustments or amendments.

Why Invest in Wells?

A population of 12,000 and just two postcodes make Wells the smallest city in England by some distance. It has held city status since the 12th century, but operates more like a market town. That smallness is the point. Housing supply is constrained by geography, conservation area restrictions, and the simple fact that there is very little developable land within the city boundary. When supply cannot expand, demand sets the floor.

The demand comes from three sources. Tourism draws visitors to Wells Cathedral, the medieval Bishop's Palace, and Vicar's Close (the oldest purely residential street in Europe). That tourism supports a hospitality and retail economy that employs locally. Retirees and lifestyle relocators are drawn to the Somerset countryside, and Wells sits at the centre of an area that stretches from the Mendip Hills to the Somerset Levels. Professional commuters use the A39 and A371 corridors to reach Bath, Bristol, and Taunton.

Between the 2011 and 2021 censuses, the former Mendip district (which included Wells, Shepton Mallet, Glastonbury, Frome, and surrounding villages) grew from 109,279 to 116,089, a rise of 6.2%. That is slightly below the England average of 6.6% for the same period. Somerset Council, created in April 2023, now administers the area as a single unitary authority.

Earnings in Somerset sit below both the regional and national averages. The median annual salary is £36,279, compared to £37,544 across the South West and £39,125 for Great Britain. That earnings gap combined with asking prices above £350,000 in both postcodes creates a market where price-to-earnings ratios exceed the national benchmark. This is not an affordability-driven market. It is a lifestyle and heritage premium that buyers accept because the alternative is to live somewhere else entirely.

The wider Somerset economy is being reshaped by two major infrastructure projects. Hinkley Point C, Europe's largest construction site, sits 30 miles to the north-west. The Agratas Gigafactory at the former Royal Ordnance site near Bridgwater is under construction 20 miles away. Both create employment that ripples across the county, supporting rental demand in smaller towns like Wells that house workers who prefer rural living.

Wells Economic Summary

- Population: 116,089 (2021 Census, former Mendip district). Growth of 6.2% from 2011.

- Median annual salary: £36,279 (Somerset), £37,544 (South West), £39,125 (Great Britain)

- Employment rate: 79.2% (Somerset), 79.3% (South West), 75.6% (Great Britain)

- Unemployment rate: 3.2% (Somerset), 3.3% (South West), 4.3% (Great Britain)

- Key employment sectors: Tourism and heritage, agriculture and food production, energy and construction (Hinkley Point C), healthcare, public services

Source: ONS Census 2021, Nomis Labour Market Profile (ASHE 2025, Employment Oct 2024-Sep 2025)

Somerset's employment rate of 79.2% matches the South West average of 79.3% and sits well above the Great Britain figure of 75.6%. The unemployment rate of 3.2% is below both the regional 3.3% and the national 4.3%. For buy-to-let investors, those numbers point to a stable tenant base. People in work stay in work in Somerset.

Regeneration and Investment in Wells

Two projects worth a combined £39bn are under construction within 30 miles of Wells. The city itself has limited large-scale development given its size and conservation constraints, but the investment story is county-wide, driven by energy and manufacturing projects that create employment across Somerset.

- Hinkley Point C (Under construction, £35bn): Europe's largest construction project, building two new nuclear reactors on the Somerset coast. The project has created over 25,000 jobs during construction and will support 900 permanent roles once operational. Workers are housed across Somerset, creating sustained rental demand in towns including Wells, Bridgwater, and Taunton. Updates at EDF Energy.

- Agratas Gigafactory at Gravity Smart Campus (Under construction, £4bn): A Tata Group subsidiary building a 40GWh battery gigafactory at the former Royal Ordnance Factory site near Bridgwater. Expected to create 4,000 direct jobs when fully operational, with thousands more in the supply chain. The scale of recruitment will increase housing demand across a county that already has limited stock. Updates at Gravity.

- The Elms, Wells (Approved, October 2025): A 100-home residential development on the eastern edge of Wells, approved by Somerset Council. The scheme includes a mix of market and affordable housing on greenfield land. For a city of 12,000 people, 100 new homes represents a meaningful addition to the housing stock. Updates at Wells Nub News.

Source: Office for National Statistics - Population for Mendip

During the 2021 Census, Wells was in Mendip district council area. As of April 1st 2023 it is now part of the new unitary Somerset council. So Census data is in Mendip and recent sold house prices are for Somerset.

Wells Property Market Analysis

When Was the Last House Price Crash in Wells?

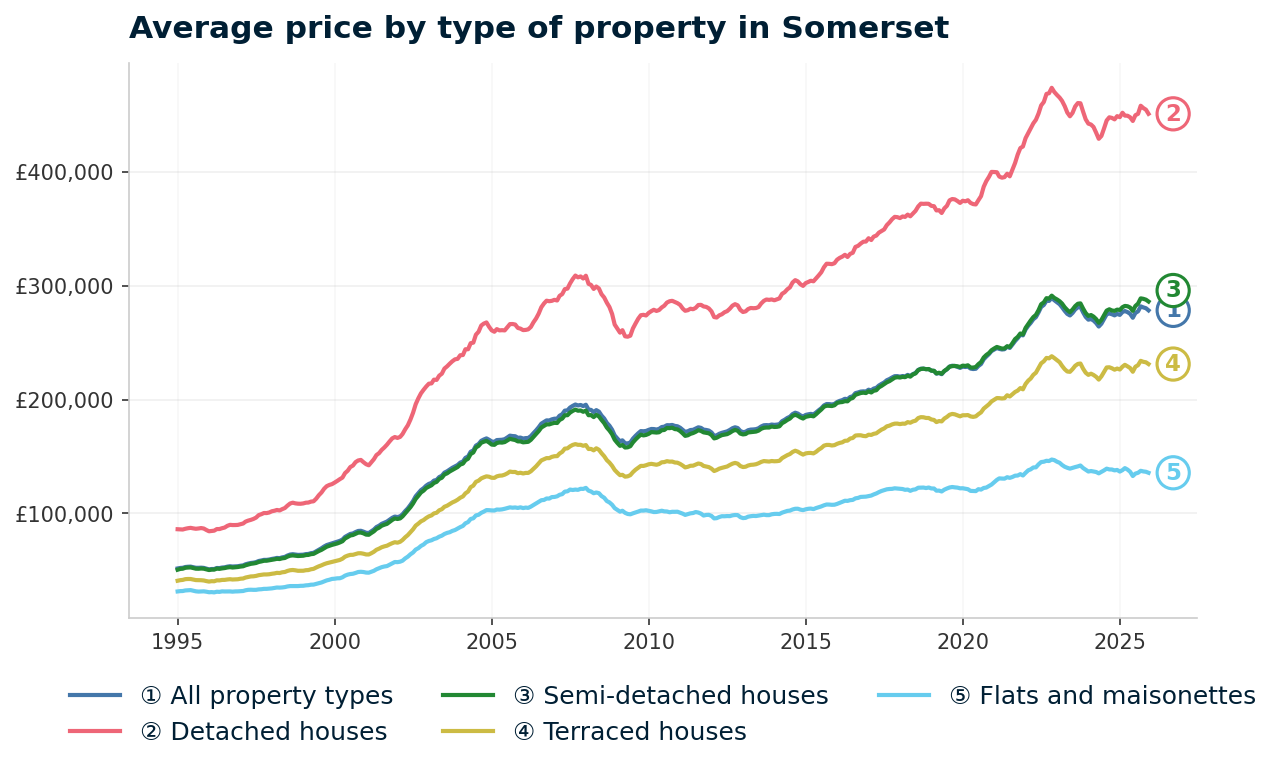

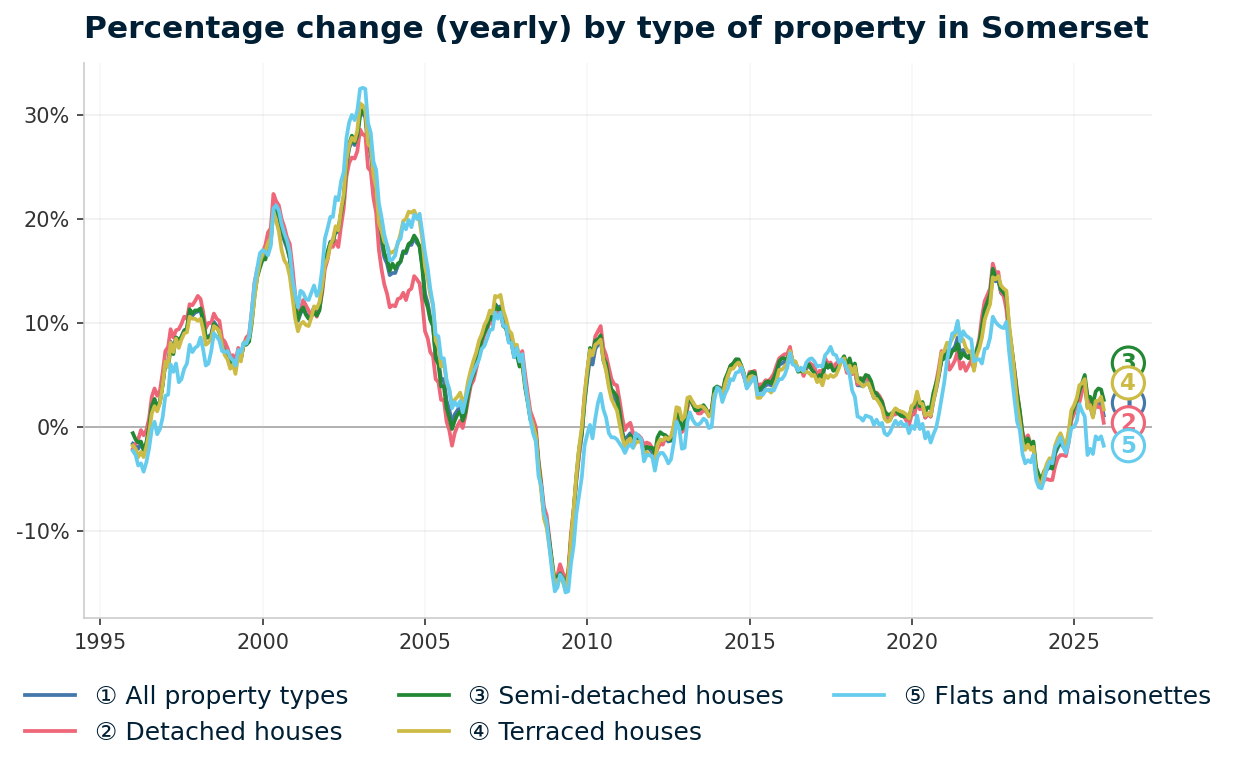

Somerset's average sold price rose 439.0% from £51,663 to £278,440 between January 1995 and December 2025, with one major crash of 17.5% in 2007-2009. All sold property prices from HM Land Registry are available at the Somerset Council local authority level. The full house price history from the HM Land Registry House Price Index runs from January 1995 to December 2025. The data shows one major crash, a prolonged stagnation, and a sharp pandemic-era surge followed by a correction.

- 1995-2000 (Steady growth): Somerset started 1995 at £51,663. By January 2000, prices had risen to £74,352. Growth was steady rather than spectacular, with an annual rate of 16.6% by early 2000 as the broader UK housing boom began to take hold.

- 2000-2007 (The boom): Prices more than doubled. From £74,352 in January 2000, Somerset reached a peak of £195,718 in September 2007. The rural South West benefited from lifestyle demand, equity-rich relocators from London and the South East, and the same cheap credit that inflated prices nationally.

- 2007-2009 (The financial crisis): From the peak of £195,718 in September 2007 to the trough of £161,559 in May 2009, Somerset lost 17.5% of its value in 20 months. The worst annual change reading was -15.3% in May 2009. Somerset's decline of 17.5% was slightly less severe than the South West region (-19.4%) and England overall (-18.2%).

- 2009-2013 (Stagnation): Somerset bounced off the trough quickly. By December 2009, prices recovered to £172,494. But then growth stalled. Prices traded sideways between £171,000 and £178,000 for four years. By December 2013, the average was £178,111. Still 9.0% below the pre-crash peak.

- 2014-2016 (Recovery): Growth returned with annual rates of 3-6%. Prices finally passed the pre-crash peak in September 2015 at £196,132. That recovery took 8 years from the September 2007 peak. Somerset recovered at a similar pace to the South West as a whole, lagging behind London and the South East where prices passed pre-crash levels by 2013-2014.

- 2017-2019 (Steady appreciation): Prices rose from £208,720 in January 2017 to £227,897 by December 2019. Consistent growth of 2-5% per year. Rural Somerset benefited from the same lifestyle appeal that drove the pre-crash boom, but at a more sustainable pace.

- 2020-2022 (Pandemic surge): The stamp duty holiday and the remote working shift accelerated growth sharply. Prices jumped from £228,956 in January 2020 to £287,389 by December 2022. That is 25.5% growth in under three years. Somerset's combination of rural character, relative affordability, and proximity to Bristol made it a prime beneficiary of the lifestyle relocation trend.

- 2023 (Rate shock): Interest rate rises cooled the market. Prices fell from £287,389 in December 2022 to £272,735 by December 2023. A decline of 5.1%. More pronounced than the national average, reflecting Somerset's exposure to mortgage-sensitive buyers who had stretched during the pandemic years.

- 2024-2025 (Stabilisation): Prices bottomed out and began recovering. By December 2025, the average reached £278,440 with annual growth of 1.1%. Somerset now sits 42.3% above its pre-crash peak.

Long-Term Property Value Growth in Somerset

- 5 years (2020-2025): +14.7% (£242,709 to £278,440)

- 10 years (2015-2025): +41.9% (£196,209 to £278,440)

- 15 years (2010-2025): +57.7% (£176,593 to £278,440)

- 20 years (2005-2025): +67.1% (£166,641 to £278,440)

- 30 years (1995-2025): +439.0% (£51,663 to £278,440)

The 2008 crash is the reference point for investors assessing downside exposure in Somerset. A 17.5% decline took 8 years to recover. That is a long wait, but the recovery came, and Somerset held up better than the South West region (-19.4%) and England (-18.2%) during the downturn. The 2023 correction of 5.1% was sharper than some expected for a rural county, but prices have since stabilised. Somerset's property market is driven by constrained supply and lifestyle demand rather than speculative development, which limits the downside in most scenarios.

Source: HM Land Registry House Price Index for Somerset, January 1995 to December 2025.

Thinking of Buying?

We have off-market investment properties averaging 8%+ annual yield.

View Property DealsSold House Prices in Wells

Somerset's Land Registry sold prices sit below the national average across every property type. The headline figure of £278,440 is 4.6% below England's £291,865 and 7.6% below the South West regional average of £301,226. That county-level discount is modest compared to many locations in the PIUK portfolio, but it masks the reality on the ground in Wells. Asking prices in both BA4 and BA5 exceed the Somerset average, meaning Wells itself trades at a premium within a slightly discounted county.

Flats show the widest gap at 38.1% below the England average. Somerset's flat stock at £135,729 is predominantly older conversions and small developments in market towns. There is no large-scale city-centre apartment market to inflate the average. The terraced discount of 5.5% and the semi-detached discount of just 1.0% tell a different story. Family homes in Somerset trade close to national levels.

| Property Type | Somerset Average | England Average | Difference |

|---|---|---|---|

| Detached houses | £451,142 | £471,667 | -4.4% |

| Semi-detached houses | £286,210 | £289,135 | -1.0% |

| Terraced houses | £231,265 | £244,830 | -5.5% |

| Flats and maisonettes | £135,729 | £219,340 | -38.1% |

| All property types | £278,440 | £291,865 | -4.6% |

Semi-detached houses show the narrowest discount at just 1.0%. Somerset semis at £286,210 are virtually indistinguishable from the England average of £289,135. Family homes are the backbone of Somerset's housing stock, and demand from owner-occupiers keeps prices close to national levels. For buy-to-let investors, the near-parity means semis offer no meaningful price advantage over buying elsewhere in England.

Detached houses at £451,142 sit 4.4% below England's £471,667. Somerset's detached stock includes everything from village cottages to larger rural properties. The discount is modest because lifestyle demand from retirees and remote workers competes directly with national price levels.

Terraced houses average £231,265, a 5.5% discount. Terraces in Somerset tend to be period properties in market towns like Wells, Frome, and Shepton Mallet. They offer lower entry prices than detached or semi-detached, and in Wells specifically, the limited supply of terraced housing near the cathedral creates a micro-premium that the county average does not capture.

The flat discount of 38.1% reflects Somerset's housing mix rather than distressed values. Unlike cities with large apartment blocks and purpose-built rental stock, Somerset's flat market is thin. Low transaction volumes and an absence of new-build apartment schemes keep the average well below national levels.

Property Data Sources

Our location guide relies on diverse, authoritative datasets including:

- HM Land Registry UK House Price Index

- Ministry of Housing, Communities and Local Government

- Ordnance Survey Data Hub

- Propertydata.co.uk

We update our property data quarterly to ensure accuracy. Last update: March 2026. All data is presented as provided by our sources without adjustments or amendments.

Price Per Square Foot in Wells

Wells's two postcodes show a spread of £38 per square foot, from £304 in BA4 to £342 in BA5. Price per square foot removes the size bias from headline asking prices. A postcode can look expensive simply because it has larger properties. This metric shows what you actually pay for space.

That 12.5% premium for BA5 reflects the Wells city centre postcode's heritage housing stock and proximity to the cathedral. BA4's lower rate covers Shepton Mallet and the surrounding villages, where properties tend to be larger and less constrained by conservation designations.

| Rank | Area | Price Per Sq Ft |

|---|---|---|

| 1 | BA4 (Shepton Mallet) | £304 |

| 2 | BA5 (Wells) | £342 |

Both postcodes sit above £300 per square foot. For context, many northern English cities have postcodes below £150. Somerset's rural character and limited new-build supply mean even the cheaper postcode commands a premium by national standards. The per-foot cost reflects heritage housing stock, period conversions, and the kind of stone-built properties that characterise the Mendip area.

Figures reflect averages across all property types and ages. Individual values depend on condition, location within the postcode, and building age.

For Sale Asking Prices in Wells

Wells's asking prices range from £350,472 in BA4 to £378,800 in BA5, with both postcodes sitting above the Somerset sold price average of £278,440. Asking prices reflect what sellers and agents think the market will pay. They are not the same as sold prices, which capture what buyers actually paid. In a market like Wells, where stock is limited and demand is driven by lifestyle choice, the gap between asking and sold prices can be narrower than in higher-volume markets.

The £28,000 gap between the two postcodes is tight. Both exceeding the county average confirms that Wells trades at a premium within Somerset.

| Rank | Area | Average Asking Price |

|---|---|---|

| 1 | BA4 (Shepton Mallet) | £350,472 |

| 2 | BA5 (Wells) | £378,800 |

BA4 at £350,472 is the lower entry point, but it is not cheap by any measure. A 30% deposit here requires £105,141. BA4 covers Shepton Mallet and the villages between Wells and Frome. The stock tends to be larger family homes and period properties on village lanes.

BA5 at £378,800 carries the cathedral city premium. Wells proper, with its medieval streets, Bishop's Palace, and proximity to Glastonbury, draws buyers who pay for location rather than square footage. The £28,328 premium over BA4 translates to an extra £8,498 on the 30% deposit.

The mean asking price across both Wells postcodes is £364,636. That figure appears in the comparison section later, where Wells is measured against Bath, Bristol, Exeter, and Salisbury.

House Price Growth in Wells

Both postcodes delivered positive five-year growth, with BA5 leading at 15.9% and BA4 at 13.4%. Growth data reveals where prices have moved over 1, 3, and 5 years. For buy-to-let investors, the five-year figure matters most because it captures a full market cycle. One-year growth can swing on a handful of transactions in a low-volume market like Wells.

The three-year figures tell a split story. BA5 grew 8.9% over three years while BA4 declined 7.6%. That divergence suggests BA4 (Shepton Mallet) was hit harder by the 2023 rate shock and is now recovering, while BA5 (Wells) held its value through the correction.

| Area | 1 Year | 3 Years | 5 Years |

|---|---|---|---|

| BA5 (Wells) | 7.1% | 8.9% | 15.9% |

| BA4 (Shepton Mallet) | 5.9% | -7.6% | 13.4% |

BA5's consistency across all three timeframes stands out. Positive growth at 1, 3, and 5 years in a market that saw a national correction is the hallmark of a supply-constrained location. Wells city has very little new housing, and properties near the cathedral rarely come to market. When they do, competition keeps prices firm.

BA4's negative three-year growth of -7.6% alongside positive one-year growth of 5.9% creates an interesting pattern. Prices surged during the pandemic stamp duty holiday, corrected through 2023, and are now recovering. An investor who bought in BA4 five years ago is sitting on 13.4% equity growth. An investor who bought three years ago is still underwater. The recovery is underway, but the data has not fully caught up.

Monthly Property Sales in Wells

Wells records 39 property sales per month across both postcodes, with BA5 at 22 and BA4 at 17. Transaction volumes show how liquid a market is. For buy-to-let investors, this is an exit strategy question. High volume and high turnover mean you can sell when you need to. In a market as small as Wells, low volume is not necessarily a warning sign. It reflects the size of the housing stock.

Turnover rates of 10-11% are modest, meaning properties change hands relatively infrequently. In a heritage market, that is expected. Owners hold for the long term.

| Area | Sales Per Month | Turnover | Asking Price |

|---|---|---|---|

| BA5 (Wells) | 22 | 11% | £378,800 |

| BA4 (Shepton Mallet) | 17 | 10% | £350,472 |

BA5's 22 sales per month is reasonable for a city of 12,000 people. It indicates a functioning market where properties do transact regularly. For comparison, individual postcodes in larger cities often see 30-50 sales per month, but they serve populations ten times larger. On a per-capita basis, Wells is active.

BA4 at 17 sales per month with 10% turnover suggests a stable, low-churn market. Shepton Mallet and the surrounding villages attract owners who stay. For investors, that means competition for stock is limited but so is the exit pool. Long-term holds suit this market better than short-term flips.

Property Data Sources

Our location guide relies on diverse, authoritative datasets including:

- HM Land Registry UK House Price Index

- Ministry of Housing, Communities and Local Government

- Ordnance Survey Data Hub

- Propertydata.co.uk

We update our property data quarterly to ensure accuracy. Last update: March 2026. All data is presented as provided by our sources without adjustments or amendments.

Wells Rental Market Analysis

For investors weighing up whether rental property is a worthwhile investment in Wells, the data below breaks down average monthly rents and gross rental yields across the city's postcodes.

Rental data is available for both of Wells's postcodes. Monthly rents range from £1,020 in BA4 to £1,152 in BA5 and gross yields range from 3.5% to 3.7%. If you are looking to build a property portfolio in the South West, Wells offers a capital preservation profile with modest but steady rental income. Browse current buy-to-let properties for sale to see what is available.

Average Rent & Gross Rental Yields in Wells

BA5 delivers Wells's highest gross yield at 3.7%, where monthly rents of £1,152 meet asking prices of £378,800. Gross rental yield is calculated from the average asking price and average monthly rent for each postcode. It does not account for void periods, maintenance, management fees, or mortgage costs. It is a starting point for comparison, not a profit forecast.

BA4 at 3.5% sits marginally lower. The yield spread of just 0.2 percentage points means the two postcodes are functionally similar for income purposes. The difference in returns comes down to entry price and growth trajectory rather than yield.

| Area | Average Monthly Rent | Average Asking Price | Gross Yield |

|---|---|---|---|

| BA5 (Wells) | £1,152 | £378,800 | 3.7% |

| BA4 (Shepton Mallet) | £1,020 | £350,472 | 3.5% |

Both yields sit below 4%, which places Wells at the lower end of the PIUK location portfolio. For context, many northern and Midlands cities deliver 5-8% gross yields at lower asking prices. Wells is not a yield play. The investment case rests on capital preservation, low void risk from constrained supply, and the lifestyle premium that underpins long-term demand.

Monthly rents of £1,020 to £1,152 are strong in absolute terms for a rural Somerset market. These reflect the quality of tenant that Wells attracts: professionals, retirees, and workers at Hinkley Point C or in Bath and Bristol who prefer a smaller city. Higher rents relative to the county average cannot push yields above 4% when asking prices exceed £350,000.

Is Wells Rent High?

Rent in Wells ranges from 33.7% to 38.1% of the local median gross monthly salary, above the general benchmark of 30%. Rent affordability matters from both sides. For tenants, it determines whether they can sustain payments long-term. For landlords, areas where rent consumes a lower share of income tend to produce more reliable tenants and fewer arrears.

The median gross weekly salary in Somerset is £697.70, which equates to £3,023 per month or £36,279 per year. This is below the South West regional median of £722.00 per week and the Great Britain median of £752.40 per week. Data from the Nomis Labour Market Profile (ASHE 2025).

Both postcodes sit above the general benchmark of 30% of gross income. That reflects the combination of above-average rents for Somerset and below-average local earnings. Tenants in Wells typically earn above the Somerset median, which the county-level salary figure does not capture.

| Rank | Area | Rent as % of Income |

|---|---|---|

| 1 | BA5 (Wells) | 38.1% |

| 2 | BA4 (Shepton Mallet) | 33.7% |

BA5 at 38.1% is the more stretched figure. Monthly rents of £1,152 against a county median monthly salary of £3,023 put the ratio well above the 30% benchmark. But tenants renting in Wells city are typically professionals working in Bath, Bristol, or the energy sector. Their actual earnings are higher than the Somerset median, which makes the headline ratio less alarming than it appears.

BA4 at 33.7% sits closer to the threshold. Shepton Mallet's lower rents of £1,020 keep the affordability ratio more manageable. For investors, the takeaway is that both postcodes serve a tenant base that earns enough to sustain these rent levels, but the county-level salary data does not reflect the true profile of Wells tenants.

Thinking of Buying?

We have off-market investment properties averaging 8%+ annual yield.

View Property DealsAre Wells House Prices High? Price-to-Earnings Ratios

Purchasing a property in Wells requires between 9.7 and 10.4 times the median annual salary of £36,279. The price-to-earnings ratio compares a postcode's average asking price to the local median annual salary. Lower ratios mean more affordable entry points relative to local wages. The national benchmark is 7.5x, calculated from England's average sold price of £291,865 against Great Britain's median annual salary of £39,125. Data from the Nomis Labour Market Profile for Somerset.

Both postcodes sit above the national benchmark of 7.5x. BA4 at 9.7x and BA5 at 10.4x mean that property prices in the Wells area are stretched relative to local incomes. This is the clearest indicator that Wells operates as a lifestyle market rather than an affordability-driven one. Buyers accept higher ratios because the alternative is not a cheaper house in Wells. It is a different location entirely.

| Rank | Area | Price-to-Earnings Ratio |

|---|---|---|

| 1 | BA4 (Shepton Mallet) | 9.7x |

| 2 | BA5 (Wells) | 10.4x |

BA4 at 9.7x is the lower ratio but still 29% above the national benchmark. Shepton Mallet is more affordable than Wells city, but it is not affordable in any absolute sense. The ratio tells you that local wages alone cannot support these prices. Demand comes from buyers with equity from other regions, retirees downsizing from higher-value properties, and professionals earning above the Somerset median.

BA5 at 10.4x reflects the Wells cathedral city premium. At £378,800 against a £36,279 median salary, the ratio is 39% above the national benchmark. For investors, this means capital growth depends on continued lifestyle demand and constrained supply rather than improving local affordability. The trade-off is lower yield but lower vacancy risk in a market where tenants compete for limited rental stock.

Deposit Requirements in Wells

Wells's 30% deposits range from £105,141 in BA4 to £113,640 in BA5, placing both postcodes in six-figure territory. The standard buy-to-let deposit is 30%. The table below reflects this benchmark, which unlocks better interest rates and a wider range of mortgage products. In a low-yield market like Wells, securing a competitive rate matters for cash flow.

The £8,499 gap between the two postcodes is modest, so the deposit alone is not the deciding factor between BA4 and BA5. The decision comes down to which postcode's growth profile and tenant mix suits the investor's strategy.

| Rank | Area | 30% Deposit Required |

|---|---|---|

| 1 | BA4 (Shepton Mallet) | £105,141 |

| 2 | BA5 (Wells) | £113,640 |

Six-figure deposits place Wells in a different bracket from most buy-to-let entry points. For comparison, many northern cities offer postcodes with 30% deposits below £50,000 and yields above 6%. Wells requires more than double that capital for a lower yield. The investment case is not about cash-on-cash returns. It is about acquiring an asset in a supply-constrained market where long-term capital preservation is supported by structural demand.

Deposit is only part of the upfront cost. Budget for stamp duty (use our stamp duty calculator for an accurate figure), legal fees, and survey costs. For a full breakdown, see our guide to buy-to-let costs. Investors with limited capital looking for stronger yields may find below market value properties offer a more accessible entry into the South West market.

What the Wells Data Tells Buy-to-Let Investors

BA5 leads across every rental metric: higher yield (3.7% vs 3.5%), higher rent (£1,152 vs £1,020), and stronger growth at every timeframe. Five-year growth of 15.9% with positive momentum across 1 and 3-year periods shows a market that held up through the 2023 correction. A 30% deposit of £113,640 buys into the Wells city postcode where constrained supply and heritage demand support long-term values.

BA4 offers a lower entry point at £350,472 but carries a weaker recent track record. The negative three-year growth of -7.6% has reversed into positive one-year growth of 5.9%, which suggests recovery is underway. BA4 covers Shepton Mallet and surrounding villages where the housing stock is larger and less constrained. The tenant profile draws from local employment and Hinkley Point C workers who prefer rural living.

The data across both postcodes positions Wells as a capital preservation market, not a yield play. Gross yields of 3.5-3.7% sit below what most buy-to-let investors target. Price-to-earnings ratios of 9.7x to 10.4x exceed the national benchmark of 7.5x. Monthly sales volumes of 17-22 are low. These are the characteristics of a market where scarcity and lifestyle demand set the floor under prices, and rental income supplements rather than drives the return.

Investors looking for investment property with higher yields will find stronger numbers elsewhere in the South West. For off-market properties in constrained markets like Wells, early access to stock can make the difference.

How Wells Buy-to-Let Compares to Nearby Areas

Wells has the lowest mean asking price (£364,636) but also the lowest top yield (3.7%) and lowest mean rent (£1,086) among five South West locations. Investors looking at Wells are typically considering the broader South West market. The table below compares Wells against four nearby locations using the same methodology: mean asking price across all postcodes, mean monthly rent across postcodes with data, and top single-postcode gross yield.

| Location | Mean Asking Price | Mean Monthly Rent | Top Gross Yield |

|---|---|---|---|

| Wells | £364,636 | £1,086 | 3.7% |

| Bristol | £372,904 | £1,777 | 8.2% |

| Exeter | £387,814 | £1,284 | 5.6% |

| Salisbury | £403,588 | £1,282 | 4.3% |

| Bath | £450,726 | £1,782 | 5.8% |

Wells has the lowest mean asking price in this group at £364,636, but also the lowest top yield at 3.7% and the lowest mean rent at £1,086. That combination defines Wells's position in the South West market. It is cheaper to buy than Bath, Exeter, or Salisbury, but the rental income does not compensate for the asking price. Bristol at £372,904 is only £8,268 more expensive but delivers a top yield of 8.2% and mean rents of £1,777. The gap in rental return per pound of capital invested is substantial.

Salisbury is the closest comparison in character: a cathedral city with heritage appeal and constrained supply. Salisbury's mean asking price of £403,588 is £39,000 higher than Wells, but its top yield of 4.3% and mean rent of £1,282 both exceed Wells's figures. Exeter and Bath offer stronger yields at higher price points, supported by university populations and deeper employment bases.

For investors comparing entry points across the South West, Wells is competitive on price but trails on rental return. The case for Wells is not about outperforming these larger markets on yield. It is about owning an asset in England's smallest city where housing supply is structurally limited. Investors seeking the best buy to let areas for income-driven strategies will find stronger numbers in Bristol, Bath, or Exeter.

Frequently Asked Questions

Is Wells a good place to live?

Wells is England's smallest city with a population of around 12,000, a medieval cathedral, the Bishop's Palace, independent shops, and direct access to the Mendip Hills. The 2021 Census recorded 116,089 people across the former Mendip district, which grew 6.2% from 2011. Somerset's employment rate of 79.2% matches the South West average, and the unemployment rate of 3.2% is below the national 4.3%.

Average asking prices of £364,636 across both postcodes reflect the lifestyle premium. The trade-off is limited public transport, no railway station, and a local economy that is smaller than nearby Bath or Bristol.

How does Wells compare to Bath for property investment?

Bath has a higher mean asking price (£450,726 vs £364,636), a higher top gross yield (5.8% vs 3.7%), and higher mean monthly rents (£1,782 vs £1,086). Bath's university population of around 30,000 students creates year-round rental demand that Wells cannot match. Bath is a deeper, more liquid market with higher rental income across a larger postcode coverage. Wells's advantage is a lower capital requirement and the scarcity premium of a micro-market with just two postcodes.

How does the Hinkley Point C construction affect the Wells rental market?

Hinkley Point C has created over 25,000 construction jobs across Somerset, with some rental demand reaching Wells 30 miles to the south-east. The £35bn nuclear construction project on the Somerset coast houses workers across the county, particularly supervisory and managerial staff who prefer smaller market towns to Bridgwater. The construction phase is expected to continue into the early 2030s. Wells's limited rental stock means even a small number of additional tenants can reduce void periods.

Can I find buy-to-let property in Wells under £200,000?

Somerset's average flat price from the Land Registry is £135,729, and individual properties in Shepton Mallet (BA4) do list below £200,000, particularly smaller terraced houses and flats. The average asking prices in this guide are £350,472 (BA4) and £378,800 (BA5), but these are postcode averages across all property types. At a £200,000 price point, a 30% deposit is under £60,000. The sub-£200,000 stock in the Wells area tends to be in Shepton Mallet or surrounding villages rather than Wells city centre, where the heritage premium pushes even modest properties above that threshold.

What is the population of Wells, Somerset?

Approximately 12,000 people live in Wells city, making it the smallest city in England. City status is conferred by the presence of a cathedral, not by population size. The wider area is covered by two postcodes: BA5 (Wells) and BA4 (Shepton Mallet). The former Mendip district, which included Wells and surrounding towns, recorded a population of 116,089 in the 2021 Census, up 6.2% from 109,279 in 2011. Somerset Council, formed in April 2023, now administers the entire county with a population of around 570,000.